When ATMs and Credit Cards Stop Working During a Blackout: The Cash Problem Nobody Plans For

When ATMs and credit cards stop working during a blackout, many families quickly discover how dependent modern life has become on electronic payment systems.

This post contains affiliate links. I may earn a small commission at no extra cost to you. Learn more.

Most people assume they will still be able to buy what they need during an emergency as long as stores remain open and products are available on the shelves. It is a reasonable assumption because modern life revolves around electronic payments. Credit cards, debit cards, mobile payment apps, online banking, and ATM networks have become so reliable that many households rarely carry more than a few dollars in cash at any given time.

That convenience works well under normal conditions, but it also creates a vulnerability that many families never consider until a major disruption occurs. During a widespread blackout, severe storm, cyberattack, or infrastructure failure, the ability to access money can become just as important as having food, water, and emergency supplies. A store may still have bottled water available. A gas station may still have fuel in its underground tanks. A pharmacy may still have essential medications in stock. None of those resources matter much, however, if payment systems stop working and customers have no alternative way to complete a purchase.

One of the biggest misconceptions about emergencies is the belief that money stored in a bank account is always immediately accessible. In reality, access to those funds depends on a vast network of electricity, telecommunications equipment, data centers, payment processors, internet connections, banking systems, and local infrastructure. When enough parts of that network fail at the same time, accessing your own money can suddenly become difficult.

History has repeatedly shown that electronic payment systems are not immune to disruption. Hurricanes, ice storms, floods, regional power failures, and communication outages have all created situations where ATMs became unavailable, card readers stopped processing transactions, and businesses were forced to operate on a cash-only basis. In some cases, outages lasted only a few hours. In others, payment problems persisted for days.

Many families focus heavily on food, water, generators, and backup power while overlooking the financial side of preparedness, even though a modest reserve of cash can become surprisingly valuable when electronic payment systems become unavailable. As discussed in Emergency Cash: How Much Should You Keep at Home?, even a small amount of accessible cash can provide important flexibility during short-term disruptions.

The good news is that preparing for payment system failures does not require large amounts of money or elaborate planning. Understanding how modern banking systems operate, where their vulnerabilities exist, and how to create a simple financial backup plan can dramatically improve your ability to navigate an emergency without unnecessary stress.

Before deciding how much emergency cash to keep or where to store it, it helps to understand why electronic payments work so well during normal conditions and why they can fail surprisingly quickly when critical infrastructure begins to break down.

Quick Answer

ATMs and electronic payment systems can stop working during a blackout if electricity, communication networks, or banking infrastructure become unavailable. Keeping a modest emergency cash reserve allows you to purchase fuel, food, medications, and other necessities when electronic payments are temporarily unavailable.

✓ Key Takeaways

- ATMs require electricity and communication networks to function.

- Credit and debit card systems may fail before stores run out of supplies.

- Cash-only businesses become more common during prolonged outages.

- Small bills are more useful than large denominations.

- Emergency cash should complement—not replace—other preparedness supplies.

Why Electronic Payments Depend on Electricity

Electronic payments often feel instantaneous and effortless. A card is inserted into a terminal, a phone is tapped against a reader, or an online purchase is completed with a few clicks. Behind that simple transaction, however, exists a highly complex system involving multiple companies, communication networks, and technological infrastructure operating simultaneously.

When a customer swipes a debit card at a grocery store, the transaction typically travels through payment processors, internet connections, banking networks, fraud detection systems, and account verification services before approval is returned to the merchant. The entire process usually takes only seconds, which makes it easy to forget how many individual components must function correctly for the transaction to succeed.

Every part of that process depends on electricity. The payment terminal requires power. The store’s internet connection requires power. Communication equipment connecting the store to the outside world requires power. Banking servers require power. Data centers require power. Cellular networks used by wireless payment systems require power. Even backup systems designed to keep these networks operating eventually depend on fuel, maintenance, and functioning infrastructure.

During a localized outage, most of these systems continue functioning because the disruption affects only a small area. Stores may switch to backup power, cellular networks may remain operational, and banks located outside the affected region continue processing transactions normally. Customers often experience little more than a temporary inconvenience.

The situation changes significantly when outages become widespread or prolonged. As more infrastructure components begin experiencing failures, the likelihood of payment interruptions increases. A store may have electricity from a generator but no internet connection. A bank may have functioning servers but lose communication with local branches. Cellular towers may continue operating temporarily but struggle as backup power systems become depleted.

Many people assume that card readers stop working simply because a store loses electricity. In reality, payment failures can occur even when a business still has lights, refrigeration, and operating cash registers. If communication networks connecting that business to payment processors become unavailable, electronic transactions may no longer be authorized.

This dependence on interconnected systems creates a vulnerability that becomes increasingly apparent during major emergencies. The more complicated the payment network becomes, the more opportunities exist for disruptions that prevent customers from accessing their funds when they need them most.

Understanding this dependency helps explain why ATMs are often among the first financial services affected during significant outages and why access to cash can become difficult much faster than many people expect.

What Happens to ATMs During a Blackout

For many people, the first response to a financial emergency is simple: go to the nearest ATM and withdraw cash. Under normal conditions, that strategy works well because ATMs provide convenient access to money at almost any time of day. During a widespread blackout, however, ATM availability can change rapidly, leaving many people unable to access their funds when demand is highest.

ATMs are often viewed as self-contained machines that simply dispense cash from an internal supply of money. In reality, they are connected to a much larger banking network that must remain operational for transactions to be approved and processed. Every withdrawal requires communication between the machine, banking systems, account verification services, and transaction processing networks. If any part of that chain becomes unavailable, the ATM may stop functioning even if it still contains cash.

When power first goes out, many ATMs immediately become unavailable because they lack dedicated backup power systems. Machines located inside banks, convenience stores, shopping centers, and retail locations often shut down as soon as the building loses electricity. Customers arriving afterward may find dark screens, disabled keypads, or error messages indicating the machine is temporarily out of service.

Some ATMs remain operational for a period of time because they are connected to backup generators or battery systems. Banks, hospitals, government facilities, and certain critical infrastructure locations may have contingency plans that allow financial services to continue operating temporarily. Even then, continued operation depends on communication networks remaining functional and fuel supplies supporting backup generators.

Another problem develops when large numbers of people attempt to withdraw cash at the same time. As news spreads about a blackout or infrastructure disruption, many individuals rush to ATMs before conditions worsen. Machines that remain operational can quickly develop long lines, and cash supplies may be depleted far faster than they would under normal circumstances.

Unlike movies that portray bank vaults filled with unlimited currency, individual ATMs contain only a finite amount of cash. They are regularly replenished through scheduled servicing and transportation logistics. During major emergencies, those replenishment schedules may be interrupted by road closures, fuel shortages, staffing problems, or communication issues. A machine that runs out of cash may remain empty until normal operations resume.

Network congestion can also become a factor. Even when ATMs still have power and cash available, banking systems may experience unusually high transaction volumes as customers attempt to access funds simultaneously. Heavy demand can slow processing times, trigger temporary outages, or cause transactions to fail altogether.

In prolonged emergencies, banks may implement additional controls designed to manage liquidity and system stability. Withdrawal limits that normally go unnoticed can suddenly become significant when families need larger amounts of cash for fuel, food, lodging, or emergency supplies. A person with substantial funds in their account may discover that accessing those funds quickly is more difficult than expected.

The most important lesson is that money stored in a bank account is not the same as cash immediately available in your hand. Bank balances represent purchasing power, but accessing that purchasing power depends on systems that may become unreliable during a major disruption. Waiting until a blackout has already begun to obtain emergency cash places you in competition with everyone else who has the same idea.

This reality explains why experienced preparedness-minded families often maintain at least a modest cash reserve before an emergency occurs. The goal is not to distrust banks or withdraw large amounts of money. The goal is to eliminate a potential point of failure by ensuring that temporary disruptions in the banking system do not immediately affect your ability to buy necessities.

Unfortunately, ATMs are only one piece of the financial system. Even if you manage to obtain cash before machines become unavailable, another challenge quickly emerges as credit card and debit card processing systems begin experiencing their own problems.

💡 Pro Tip

Do not wait until an emergency begins to withdraw cash. Once long lines form at ATMs or banking networks experience disruptions, accessing your own money may become much more difficult.

Why Credit and Debit Card Systems Fail During a Blackout

Many people assume that if an ATM is unavailable, they can simply continue using a credit card or debit card for purchases. After all, card payments have become so common that many households rarely carry cash anymore. Unfortunately, electronic payment systems are vulnerable to many of the same infrastructure problems that affect ATMs, and in some situations they can fail even faster than people expect.

Every time a card is inserted, tapped, or swiped, a series of electronic communications takes place behind the scenes. The payment terminal must send information through a network connection to a payment processor. That processor communicates with banks and financial institutions to verify available funds, confirm account status, perform fraud checks, and approve the transaction. The approval then travels back through the system to the merchant. The process usually takes only a few seconds, making it appear simple even though it relies on a complex chain of technology.

When electricity is interrupted, any link in that chain can become a problem. A store may have functioning cash registers but lose internet connectivity. Cellular payment terminals may operate briefly but become unreliable if communication towers lose power. A business running on generator power may continue serving customers while payment processing systems located elsewhere experience outages. From the customer’s perspective, the card simply gets declined even though funds are available.

Large retailers sometimes have sophisticated backup systems that allow limited operations during disruptions, but smaller businesses often have fewer options. Local grocery stores, convenience stores, restaurants, pharmacies, and gas stations may find themselves unable to process electronic payments despite still having products available for sale.

One challenge that surprises many people is that payment failures do not always happen immediately. A business may continue accepting cards for several hours after a blackout begins because backup systems remain operational. Customers become accustomed to transactions working normally and assume there is no problem. Then, as batteries discharge, communication systems fail, or network congestion increases, card processing suddenly stops. People who delayed obtaining cash may discover that their options have become much more limited.

Regional outages create another layer of complexity. A store with generator power may continue operating while the banking systems serving that region experience interruptions elsewhere. In that situation, lights remain on, employees continue working, and products remain available, yet electronic payments cannot be completed because the communication infrastructure connecting those systems has been disrupted.

Even mobile payment applications depend on the same underlying infrastructure. Services such as digital wallets, payment apps, and contactless transactions may appear different from traditional card payments, but they still require functioning communication networks, banking systems, and transaction processors. If those supporting systems become unavailable, digital payment methods often fail alongside conventional credit and debit cards.

Another factor is customer behavior. As outages continue, transaction volumes often increase dramatically. People rush to buy supplies, fuel, batteries, water, and other necessities. The sudden surge in activity places additional strain on payment networks that may already be operating under difficult conditions. Slower processing times, connection errors, and failed transactions become more common.

The average person rarely thinks about how dependent modern commerce has become on electronic infrastructure until those systems stop functioning. For decades, cash served as the primary backup method when technology failed. Today, many individuals carry little or no physical currency, which means even short-term payment disruptions can create significant inconvenience.

Preparedness is not about assuming that every blackout will lead to financial chaos. Most outages are resolved quickly and payment systems recover without major issues. The concern is that widespread or prolonged disruptions can expose weaknesses that are easy to ignore during normal conditions. Having a backup plan allows you to continue purchasing necessities without relying entirely on technology that may be temporarily unavailable.

The importance of that backup becomes especially apparent during the first day of a major blackout, when confusion, uncertainty, and rapidly changing conditions cause many people to make financial decisions under pressure.

📌 Did You Know?

Many payment terminals continue working for a short time on battery backup, but they can still fail if internet service, cellular networks, or payment processors become unavailable.

The First 24 Hours: Confusion at Stores and Gas Stations

The first day of a major blackout is often characterized by uncertainty rather than outright shortages. Most businesses still have inventory available, fuel remains stored in underground tanks, and many services have not yet been significantly affected. The primary challenge is that people do not know how long the outage will last, which often causes a sudden increase in demand for critical supplies.

As news spreads about a large-scale power failure, stores frequently experience a rush of customers seeking bottled water, shelf-stable foods, batteries, flashlights, medications, ice, fuel containers, and other emergency essentials. Checkout lines grow longer as more people attempt to purchase supplies at the same time.

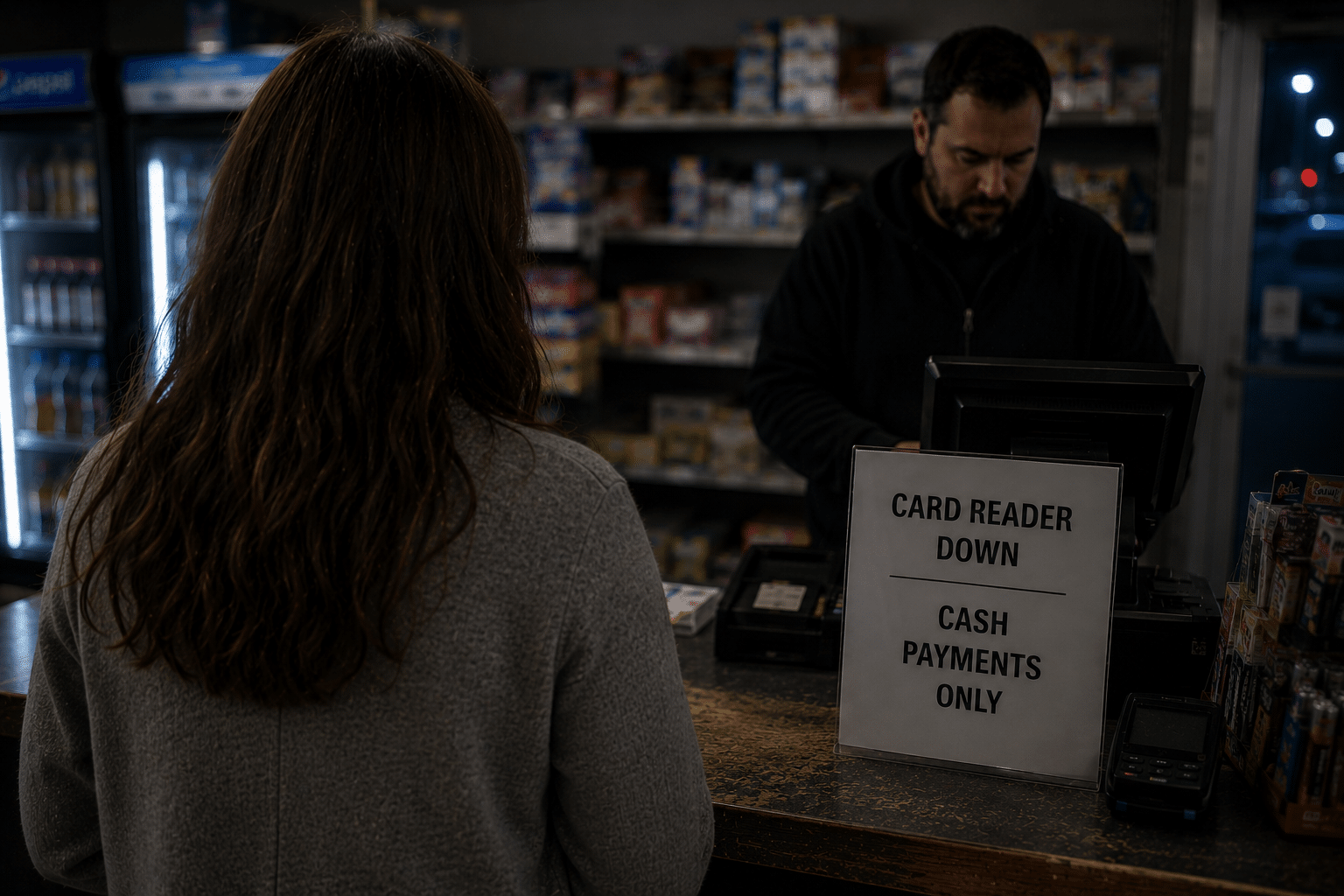

If electronic payment systems remain operational, transactions may continue normally for a while. Customers often assume conditions will remain stable and focus primarily on obtaining supplies. Problems begin emerging when communication networks become overloaded, backup power systems are exhausted, or payment processors experience disruptions. Businesses that accepted cards earlier in the day may suddenly switch to cash-only operations with little warning.

This transition can create frustration for both customers and employees. A shopper may spend considerable time gathering supplies only to discover that electronic payments are no longer being accepted. Employees often have little control over the situation because the issue exists within external payment networks rather than the store itself.

Gas stations frequently become one of the most visible examples of payment-related disruptions during blackouts. Fuel quickly becomes a priority for households attempting to travel, operate generators, check on relatives, or prepare for an extended outage. As explained in How Long Will Gas Stations Work During a Blackout?, payment systems often become just as important as fuel supplies themselves.

A station may have thousands of gallons of fuel underground, but dispensing that fuel requires electricity to operate pumps and payment equipment. Some stations use generators to maintain operations temporarily. Others shut down completely until power is restored. Even when fuel pumps continue working, electronic payment processing may become unreliable if communication networks are disrupted.

Customers who have cash available generally have more flexibility during these situations. They can adapt quickly when businesses transition to cash-only policies and avoid some of the delays associated with payment system outages. Those relying entirely on cards may find themselves searching for operational ATMs at the same time thousands of other people are doing exactly the same thing.

The first twenty-four hours are often manageable for prepared households because supply chains have not yet been significantly affected. The larger challenge emerges when outages continue for multiple days and both financial systems and physical supplies begin experiencing increasing pressure.

⚠ Important Warning

Do not assume that having money in your bank account guarantees immediate access to it. During widespread outages, ATMs, payment processors, and communication networks can all become unavailable at the same time.

What Happens When the Outage Lasts Several Days

The longer a blackout continues, the more noticeable the effects become across every part of daily life. During the first day, most people focus on immediate inconveniences such as lost lighting, spoiled food concerns, and temporary interruptions to normal routines. By the second, third, and fourth days, attention often shifts toward obtaining supplies, preserving resources, and managing uncertainty about when services will return.

This is where payment problems can become more serious. A short disruption may simply delay purchases for a few hours. A prolonged outage can create a situation where people still have money in their bank accounts but face increasing difficulty using it.

As backup generators consume fuel, businesses must make decisions about what services they can continue providing. Some stores may reduce operating hours. Others may close entirely. Communication networks that remained functional during the early stages of the outage may begin experiencing additional failures as battery systems are depleted and maintenance crews struggle to keep up with demand.

Even businesses that remain open often operate under challenging conditions. Inventory may be arriving more slowly. Employees may be dealing with their own emergency situations at home. Deliveries may be delayed by fuel shortages, damaged infrastructure, or transportation disruptions. Every additional day places more strain on systems that were designed for normal operating conditions rather than emergency demand.

Financial transactions become increasingly complicated when communication networks become unreliable. A store may be willing to accept cards one moment and unable to process transactions the next. Customers who assume electronic payments will continue functioning normally can find themselves in difficult situations when systems suddenly become unavailable.

Food purchases provide a good example. Even when stores still have inventory available, purchasing those supplies can become difficult when electronic transactions are unavailable, a challenge that often develops alongside the supply disruptions discussed in How Long Will Grocery Stores Have Food During an Emergency?.

Pharmacies can face similar challenges. Prescription medications may still be available, but processing insurance information, accessing patient records, and verifying payments often depend on functioning communication systems. Patients who rely entirely on electronic transactions may encounter delays at precisely the moment they need essential medications most.

Another issue that develops during prolonged outages is uncertainty. When people do not know whether power will return in a few hours or several more days, purchasing behavior changes. Households become more cautious about conserving resources while simultaneously trying to obtain additional supplies. This increased demand can place further pressure on businesses already operating under difficult circumstances.

Cash often becomes more valuable during this stage because it removes one layer of uncertainty from the transaction process. A merchant does not need to verify network connectivity, wait for authorization, or troubleshoot payment terminal errors. The exchange is immediate and straightforward. While cash cannot solve every problem, it can simplify transactions when technology becomes unreliable.

Communities that experience hurricanes, severe ice storms, flooding events, and other large-scale disasters frequently report periods where cash became the preferred or only practical method of payment. These situations rarely last forever, but they occur often enough to justify including financial preparedness as part of a broader emergency plan.

The goal is not to assume that society will suddenly abandon electronic payments. The goal is to recognize that temporary interruptions are possible and that having alternatives available reduces stress during already challenging circumstances. A household that has food, water, backup lighting, and a modest cash reserve is typically better positioned than one relying entirely on systems outside its control.

This naturally leads to one of the most common questions people ask when discussing emergency preparedness and financial resilience: exactly how much cash should be kept at home in case electronic payment systems become unavailable?

🚨 Imagine This…

Three days into a regional blackout, your local grocery store still has food on the shelves but announces it can only accept cash because electronic payments are offline. While many customers leave empty-handed, your family has a small emergency cash reserve and is able to purchase the supplies you need.

How Much Cash Should You Keep at Home?

There is no universal amount of emergency cash that works for every household. Family size, location, transportation needs, medical requirements, and preparedness goals all influence how much money may be useful during a disruption. The objective is not to store large sums of currency at home but rather to maintain enough accessible cash to cover essential expenses if electronic payments become temporarily unavailable.

A practical way to approach the question is to think about the purchases most likely to occur during the first several days of an emergency. Fuel is often near the top of the list. A family may need gasoline for evacuation, commuting, operating generators, checking on relatives, or traveling to locations where services remain available. Food purchases may also become necessary if existing supplies are limited or the emergency lasts longer than expected.

Some households may need cash for prescription medications, temporary lodging, emergency repairs, transportation expenses, pet supplies, or other critical needs. The amount required depends largely on personal circumstances rather than a single preparedness formula.

For many families, a reserve ranging from a few hundred dollars to several hundred dollars provides a reasonable starting point. The exact number matters less than the existence of a plan. Even a relatively modest amount of cash can significantly improve flexibility during a short-term outage when payment systems are experiencing disruptions.

One mistake people sometimes make is focusing exclusively on total dollar value while ignoring practicality. A stack of large bills may technically contain enough money, but it may not be particularly useful if local businesses cannot make change. Small and medium denominations often provide more flexibility than larger bills during emergencies.

Emergency cash should also be viewed as one component of a broader preparedness strategy rather than a standalone solution. Money cannot replace stored food, emergency water, backup lighting, medications, fuel reserves, or communication equipment. Instead, it complements those resources by providing additional options when unexpected needs arise.

Households that already maintain emergency supplies often discover that they require less emergency cash than those who depend entirely on purchasing necessities after a disaster begins. The more prepared you are beforehand, the less pressure there is to spend money during the critical early stages of an emergency.

Another consideration is accessibility. Emergency cash should be stored in a secure location that remains accessible during power outages and other disruptions. If obtaining your cash requires electricity, internet access, or travel through hazardous conditions, it may not provide the benefit you intended.

The purpose of maintaining emergency cash is not fear or distrust. It is simply recognizing that financial systems, like all infrastructure, can experience temporary interruptions. A small reserve provides an additional layer of resilience that may prove valuable when other options become limited.

Once people decide how much cash to keep available, the next question becomes equally important: what types of bills should actually make up that emergency reserve?

The Best Types of Bills to Keep

Many people focus entirely on how much emergency cash to store while overlooking the importance of bill denominations. During a blackout or infrastructure disruption, having the right mix of currency can be almost as important as the total amount available.

Small businesses operating under difficult conditions may have limited access to change. Cash registers may be functioning manually, replacement cash may be difficult to obtain, and employees may be trying to process transactions as quickly as possible. Presenting a large bill for a small purchase can create complications that slow down the transaction for everyone involved.

For this reason, many preparedness-minded households prefer to keep a combination of smaller denominations. Tens, twenties, fives, and even a limited number of one-dollar bills provide flexibility for purchasing fuel, food, batteries, ice, medications, and other necessities without depending on a business having adequate change available.

A balanced approach often works best. Larger bills can reduce storage space and make it easier to maintain an emergency reserve, while smaller bills improve practicality during actual transactions. The exact mix is less important than ensuring you are not dependent entirely on large denominations.

It is also wise to periodically inspect stored cash for damage and ensure that family members know where it is located in case the primary decision-maker is unavailable during an emergency.

What Cash Can and Cannot Solve

Emergency cash can provide important flexibility during a blackout, but it is not a solution to every problem. Having money available may help you purchase fuel, food, batteries, medications, or other necessities when electronic payment systems are unavailable. It can also reduce stress by giving you additional options during the early stages of an emergency.

At the same time, cash cannot create supplies that no longer exist. If a store has completely sold out of bottled water, fuel, generators, or prescription medications, having extra money will not make those items magically reappear. Supply shortages and infrastructure disruptions can affect everyone regardless of their financial situation.

This is one reason preparedness experts consistently emphasize storing essential supplies before an emergency occurs. Cash works best when it complements preparation rather than replacing it. Families that already have food, water, lighting, backup power, and basic medical supplies typically face far less pressure during the first days of a disruption.

Building those supplies ahead of time is often easier than trying to purchase them during a crisis, which is why many households begin with a simple Emergency Preparedness Plan before focusing on more advanced preparations.

Another limitation is security. Large amounts of cash can be lost, stolen, damaged by fire, or destroyed by flooding. Maintaining a reasonable emergency reserve is very different from keeping excessive amounts of currency at home. The goal is practical preparedness, not attempting to replace traditional banking.

Think of emergency cash as another backup system. Just as a flashlight provides backup lighting and stored water provides backup hydration, cash provides backup purchasing power when normal payment methods become unavailable.

Building a Financial Backup Plan

Financial preparedness is most effective when it becomes part of a larger emergency plan rather than a standalone strategy. A household that has cash available but lacks communication plans, emergency supplies, and contingency procedures may still struggle during a prolonged outage.

A simple financial backup plan can include maintaining a modest emergency cash reserve, keeping important financial documents organized, monitoring account access methods, and ensuring family members understand how to access essential resources during an emergency.

It is also worth considering how family members would communicate if normal services became unreliable. Financial preparedness works best when it is integrated into a broader household preparedness strategy, including the communication procedures outlined in Family Emergency Communication Plan (Step-by-Step).

Reviewing your plan periodically helps ensure it remains practical. Family needs change over time, expenses increase, and new risks emerge. A preparedness plan that worked five years ago may not fully address current circumstances.

The objective is not perfection. It is simply reducing dependence on any single system that could fail during an emergency. The more backup options your family has available, the easier it becomes to adapt when conditions change unexpectedly.

🛒 Recommended Financial Preparedness Gear

Financial preparedness involves more than simply keeping cash at home. These products help protect your emergency funds, maintain communication, and keep essential devices operating during extended power outages.

Fireproof Waterproof Document Safe

Protects emergency cash, important documents, passports, insurance paperwork, and other valuables from fire, water damage, and theft.

Emergency Weather Radio

Provides NOAA weather alerts and emergency broadcasts when internet service and cellular networks become unreliable, helping you stay informed while financial systems recover.

Jackery Portable Power Station with Solar Panel

Provides backup power for phones, communication devices, and other electronics used to monitor banking information, emergency alerts, and family communications.

☑ Financial Preparedness Checklist

- ☑ Keep a modest emergency cash reserve.

- ☑ Include small bills for everyday purchases.

- ☑ Store cash securely with important documents.

- ☑ Review emergency spending priorities.

- ☑ Maintain backup communication methods.

- ☑ Keep vehicles fueled before storms.

- ☑ Review your financial plan regularly.

📚 Continue Reading

Continue strengthening your financial and blackout preparedness with these related guides.

Frequently Asked Questions

Will credit cards work during a blackout?

Sometimes. Card payments can continue briefly if stores, communication networks, and payment processors remain operational. During larger or longer outages, payment systems often become unreliable.

Can ATMs work without electricity?

Most ATMs stop working when power is lost unless they are connected to backup power and communication networks remain available.

Should I keep emergency cash at home?

Many preparedness-minded families maintain a modest cash reserve to cover fuel, food, medications, and unexpected expenses during temporary disruptions to electronic payment systems.

Final Thoughts

Modern banking and payment systems are remarkably reliable, which is why many people never consider what might happen if they suddenly become unavailable. Yet every electronic transaction depends on electricity, communications infrastructure, data networks, and financial systems working together at the same time.

Most blackouts will not lead to widespread financial disruption, but larger and longer-lasting outages can create situations where accessing money becomes far more difficult than expected. ATMs may stop working, card readers may fail, and businesses may shift to cash-only operations with little warning.

A modest emergency cash reserve cannot solve every problem, but it can provide valuable flexibility when electronic payment systems become unreliable. Combined with food storage, water supplies, backup power, and a well-developed preparedness plan, it becomes another tool that helps families navigate uncertain situations more confidently.

Payment systems represent only one piece of a much larger infrastructure network, and understanding how those systems interact with other critical services becomes easier after reading What Stops Working First in a Long-Term Blackout?.

The best time to prepare for a payment disruption is before one occurs. Once ATMs stop dispensing cash and card networks become unreliable, the opportunity to prepare has already begun to disappear.